The Bitcoin Bridge Thesis

An obvious solution that needs to be shared.

Thank you for finding your way here. Hopefully you have a sense of what’s happening in Clown World. If you do, then what I’m going to share will make a lot of sense to you but be prepared to have your convictions tested.

Important disclosure: My financial strategy was developed for my situation alone and while it is simple to adopt, the best advice is always to do your own research and be your own best advocate. Don’t follow the crowd, and most importantly: “Don’t trust, verify!”

Let’s begin.

First, my credentials.

I’ve been in the life insurance industry since my 20’s teaching an Austrian economic strategy of warehousing my wealth through the ownership of Whole Life policies. You can read more about me here.

If Malcolm Gladwell is correct about spending 10,000 hours on a subject qualifies a person as an expert, then I’ve put in multiple decades of time in learning and applying my trade to be considered an expert on life insurance.

According to the latest statistics, 52% of American have at least one of type of life insurance product. That means 52% of American value having death benefit protection, and if these same people have done some studying, it’s possible their life insurance does a lot more than just provide a death benefit.

The problem is most people don’t study. They don’t take ownership of their financial life and most will never open another book after graduating from high school. I don’t like being the person to say it, but owning life insurance is a homework test.

When you do your homework, understanding what type of policy to buy is a no brainer: convertible term and/or whole life. Avoid any and all flavors of universal life policies because of the high lapse rate inherent in them due to misleading sales tactics, underfunding, increasing costs of insurance, and potential underperformance.

But… at least 52% of Americans have enough sense to buy some sort of protection on their life. Yes, this could be a lot higher but it gives me hope for the Bitcoin journey I’d like to share with you.

My logic goes like this: if you believe in protecting your livelihood so much that you are willing to pay a premium for life insurance protection, you are one step closer to saving additional “confetti” dollars in the best money ever created. Bitcoin is the ultimate insurance protection against the endless government transfer of your wealth to them via inflation.

Based on my experience, here’s one fundamental truth about life insurance I’ve learned along the way and it also applies to bitcoin:

Most people’s understanding of life insurance is based on on someone else’s misunderstanding.

I encounter this obstacle almost every day. That’s why it’s equally important to do your homework on Bitcoin. Do not rely on other people to do your own thinking.

People don’t know what they don’t know, including traditional Wall Steet advisors, and being misinformed is sometimes worse than being uninformed. Misinformed people have a higher hurdle to learning because their bias gets in the way.

So if what you read on this Substack challenges what you think you know about life insurance and bitcoin, that’s good. You’re in the process of learning and possibly overcoming your own bias with what you thought you previously knew.

I invite you to ask me anything about life insurance and Bitcoin. Don’t be embarrassed if you have a seemingly silly question. I rarely get a question I haven’t heard hundreds of times. And, by chance, if you do stump me, I know people who have the answer if I don’t. Industry conferences and masterminds are great primarily for this reason.

With regards to my experience with Bitcoin, I’m almost a decade into it. Call me lucky for being relatively early, but that would be incorrect. I was ready for the solution to fiat for a long time thanks to books like The Creature From Jekyll Island and End The Fed, so I intuitively knew Bitcoin was special when I first heard about it. Separate money and state?!? Absolutely! It just took me another 6 years to:

grasp that Bitcoin could or would actually succeed and

that everything not bitcoin is a shitcoin pretending to be bitcoin.

Once I absolutely realized bitcoin was Money You can’t F*ck With in early 2021, I decided to dedicate as much time to it as possible to learning as much I could. Fast forward to the present and my journey down the rabbit hole is insatiable.

From philosophy, history, real economics (not psuedoeconomics promoted by governments and its shills), and even Christianity, there is seemingly nothing that Bitcoin doesn’t touch on that doesn’t interest me. My daily routine: walking 2 hours while listening to Bitcoin podcasts during those walks, listening when I exercise and run errands; I listen sometimes up to 6 hours a day. If Guy Swann, host of Bitcoin Audible, “has read more about Bitcoin than anyone you know”, I’ll go out a limb and say since 2021 few have consumed more Bitcoin podcast content than me.

Does this make me a full-fledged Bitcoin expert? Not in any certified way, but I’m confident I can speak more intelligently about bitcoin than 99% of the population. More importantly, because I better understand bitcoin and the incentives produced by fiat money than your next door neighbor, I can see through lies corporate media and governments serve on the daily. I can’t be gaslighted. At least, not easily. That is the gift, and perhaps the curse, of Bitcoin. You see the world with new eyes and once you see the truth, you can’t unsee it. You absolutely cannot go back to the fiat lie. Fair warning, I suppose.

Now to my thesis

What I do with my savings is built on a foundation of certainty and predictability no matter what’s happening in the economy or Clown World at large.

How do we find certainty in uncertain times? Simple. We choose things that are immutable and set in stone. We “bet” on things that are, as Jeff Bezos says, are "stable in time."

Well, to paraphrase Jeff Bezos a bit, and based on what I already knew about Whole Life and Bitcoin I asked:

What are three things I am confident won’t change in 10 or 1000 years?

The need for the sound money (utilizing the best denominator): Bitcoin.

The need for access to tax-free cash, without interrupting the compounding wealth curve: Whole Life policy loans.

Solving for a lifetime need of financing via the banking process: Whole Life… and eventually Bitcoin when financial institutions are able to collateralize it for loans.

What I’ve realized is that Bitcoin and Whole Life represent the two best savings technologies ever created AND they each do something the other cannot do separately. Together they accomplish all 3 things that a person will always need. Together is the key word there!

I believe once you understand Bitcoin and Whole Life, you’ll want to own both. The reason is simple:

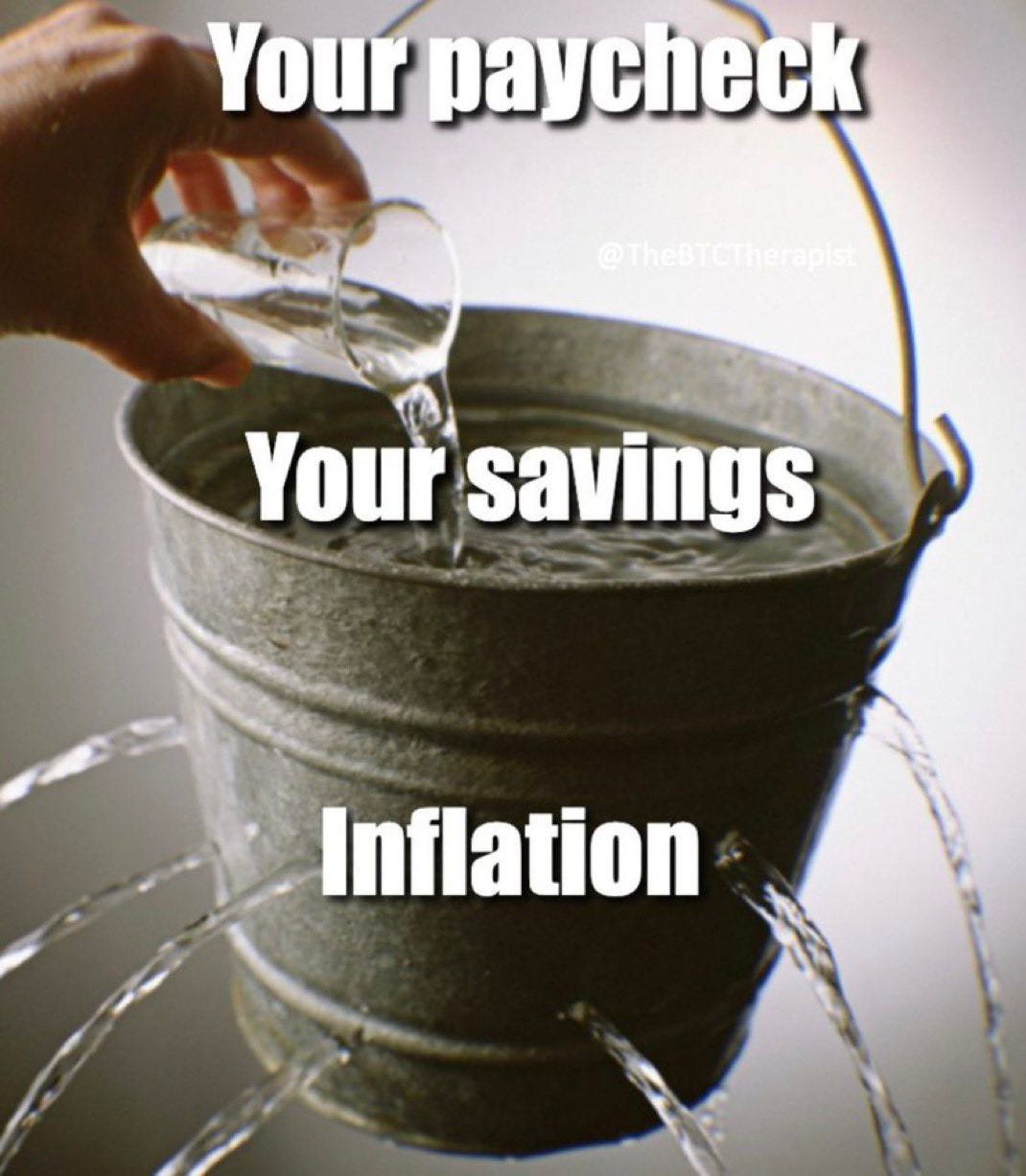

In a world of broken money where governments and central banks plunder our wealth with an endless supply of fiat money, the hardest money (Bitcoin) is the best insurance policy (and investment) against the neverending loss of your purchasing power in fiat terms.

Step #1: Study Bitcoin (Check out my posts: Starting Point I & II)

Step #2: “Buy some in case it catches on.”

January 10, 2024, Spot Bitcoin ETF’s approved by SEC.

May 16, 2024, so called “boring money” is now in Bitcoin. Wisconsin pension fund now includes bitcoin. Looks like pension funds have started doing their homework!

November 4, 2024, first UK pension fund invests in Bitcoin

Do you see the trend?

Even if you currently happen to be fully orange-pilled and realize Bitcoin is the solution to the dollar losing purchasing power forever, no one has a foolproof plan for what to do in the meanwhile saving in bitcoin as we wait for the rest of the world to get up to speed with this Once In A Species Discovery.

The greatest challenge I see, even from those who best understand Bitcoin, is that no one has a crystal ball for how long the transition to a sound monetary system will take.

How long will the Dollar will be king? Well, how long did it take for the Soviet Union to go bankrupt? Gradually for decades, then suddenly. We could be dealing with higher than normal inflation for a very, very long time and we need an uncomplicated yet bulletproof plan for the current financial purgatory as we transition towards the next monetary system.

This unknown is why I believe there is one common sense and fail safe strategy to bridge the present to the future. If you are married and/or have kids, or perhaps plan to have kids, I think it’s irresponsible to be 100% long into Bitcoin so you should have a portion of your savings in another vehicle. I believe Whole life is that other vehicle specifically for fiat savings. At minimum, it serves as a superior cash solution than a rainy day savings account at your local fractionally reserved bank.

In the fiat world, this is what I’ve been saying for almost 20 years:

The best fiat warehouse for cash and financing outside of the traditional rails of fiat banking system is a Whole Life policy housed in privately owned, mutual-based (policyholder owned) life insurance companies.

I’d like you to understand a few basic things about Whole Life.

It’s fundamentally about a fixed, immutable ledger. Sound familiar?

It’s rooted in Austrian economics as a full reserve system. Sound familiar?

It’s property. It’s a commodity. It’s intangible. It uses low-time preference. It’s private. It eliminates traditional banking intermediaries. It combines wealth preservation and legacy planning. It’s absolutely scarce (how limited is our time on earth?). I have a much longer list but…

If you know Bitcoin, this should all sound familar

In short, Whole Life is a financial unicorn hiding in plain sight for 170+ years and the average person to this day fails to grasp its full value.

And here’s what Whole Life does that Bitcoin cannot ever do.

It simultaneously creates a present Cash Value and future value called the Death Benefit (both are contractually guaranteed and backed by fully reserved life insurance companies… the complete opposite of fractional reserve banks).

Without need for additional 3rd parties, non-MEC Whole Life (i.e. properly structured) policies guarantee tax-free policy loans for any reason as quickly as 3-5 business days. None of the hoops to jump through like with a traditional bank loan. Tax-free loans are embedded into the IRS tax code section 7702. Loans are guaranteed and can be repaid on any schedule you choose, including no repayment ever at all.

The 1st point is what I’ve used to anchor my life in the present to build a rock solid financial foundation, as much as it is realistically possible, in a fiat world of compounding annual inflation.

“You’ll never be in worse position by having access to cash.”

Having available cash values in a Whole Life policy has provided me a superior emergency fund to bank money while giving me and my family more economic bang for my buck. It’s why I believe every disciplined household should have a Whole Life policy, at a minimum, to be used as an emergency fund.

And the present Cash Values of a Whole Life policy are something I never have to waste once second worrying about market loss. As a non-correlated asset, it is insulated from the daily chaos of an uncertain world. And should I die prematurely, the death benefit pays off any policy loans and guarantees a tax-free death benefit (estate tax-free up to present IRS guidelines).

In contrast, bitcoin has no guaranteed future value. The price of bitcoin today $66k~ could be anything in fiat paper terms next week, next year, or even 20+ years from now. We just don’t know.

Not so with a Whole Life policy. As time goes on, the growing cash values in a whole life policy become an opportunity fund for anything life has thrown my way:

Divorce, medical bills, college tuition, down payment for my home, car financing, and best of all investing (real estate, private business ventures, even bitcoin).

On point #2, I can currently borrow against my Whole Life policies at simple interest between 5-7.45%. Current Bitcoin lenders like Unchained and LEDN offer loans against bitcoin above 12% making banking (borrowing) against a Whole Life policy a no-brainer alternative. Plus, I’d rather using fiat as collateral than beautiful, pristine bitcoin. Eventually, better options for banking with bitcoin will be a reality and likely sooner than you realize but we aren’t there yet…

TLDR: Whole Life with a PUA rider bridges the present to the future Bitcoin world by providing you with both present (cash value) and future (death benefit) in fiat values with guaranteed growth and liquidity outside of the fractional reserve banking system. Establish what you need for a fiat rainy day fund in Whole Life policy that protects your family and your ability to be your own bank. Then also study Bitcoin while you stack satoshi’s (the smallest unit of bitcoin is 0.00000001) on a weekly basis as the ultimate insurance policy against to protect against ongoing loss of fiat purchasing power. In my own lingo: stack sats and PUA.

The formula is simple: WL + BTC = Freedom

Full disclosure: you can absolutely get by without a Whole Life policy and just save in bitcoin. There are plenty of inferior options like a fiat bank line of credit or brokerage margin account as a fiat alternative to banking with Whole Life, but if you’re in good health and can qualify, you should absolutely think about re-positioning a portion of your emergency fiat cash savings in a private, guaranteed Whole Life contract with a mutual based life insurance company, versus keeping it in your fractional reserve fiat bank where, unintentionally, you are actually contributing to the inflation problem!

How much “dirty” fiat should you keep in a Whole Life policy? That’s a topic for another post but it’s like asking how much bitcoin should you own. The answer is simple:

The more you know about Bitcoin, the more you will own.

As my mentor would say often: “If you don’t understand the problem, you won’t understand the solution.”

My strategy of paying premiums and stacking sats is simple and easy. It’s also peaceful. I sleep well at night.

If you have questions, please follow and send me a DM on X/Twitter. Until the next post…

Cheers,